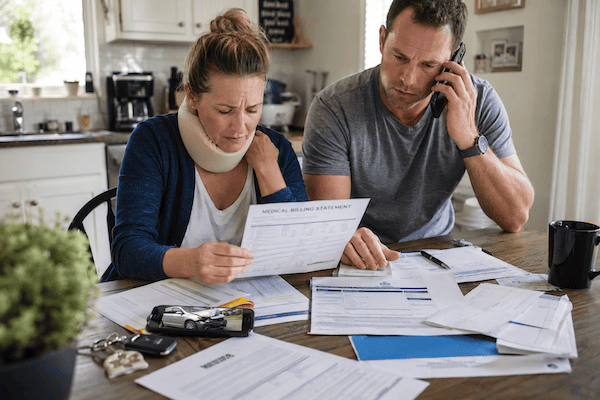

Dealing with the aftermath of a car accident is stressful enough when you are trying to heal. But when medical bills start arriving, the pressure can feel overwhelming. You may be wondering who pays for the emergency room visit, imaging, follow-up appointments, physical therapy, and any future care you may need.

In Florida, medical bills after a crash are not always handled the way people expect. The other driver’s insurance company usually does not pay your bills as they come in. Instead, your own insurance coverage typically applies first, and strict rules affect when and how those benefits are available.

Understanding how medical bills get paid after a Pensacola car accident can help you protect your health, your finances, and your legal claim.

Key Takeaways

- Florida’s no-fault system means your own Personal Injury Protection, or PIP, coverage usually pays first.

- You must seek medical treatment within 14 days of the crash to preserve PIP benefits.

- PIP generally covers 80% of reasonable medical expenses up to $10,000, but serious injuries can exceed that quickly.

- The at-fault driver’s insurance usually addresses medical bills through a settlement, not by paying each bill as it arrives.

- Other payment sources may include health insurance, MedPay, medical liens, bodily injury liability coverage, or UM/UIM coverage.

Florida’s No-Fault System: Where Payment Starts

Florida is a no-fault insurance state. This means your own auto insurance policy is usually the first source of payment for medical treatment after a crash, regardless of who caused the accident.

Every Florida driver is required to carry Personal Injury Protection coverage. PIP generally covers 80% of reasonable medical expenses and 60% of lost wages, up to $10,000 in total benefits.

For minor injuries, PIP may cover a meaningful portion of the bills. But for serious injuries, that coverage can run out quickly. A single emergency room visit, ambulance ride, MRI, CT scan, or specialist appointment can use up much of the available coverage.

The 14-Day Rule

To qualify for PIP benefits, you must seek medical treatment within 14 days of the accident. If you wait longer than 14 days, your insurance company can deny PIP benefits entirely.

This is important even if your symptoms seem minor at first. Neck pain, back pain, headaches, dizziness, and soft tissue injuries may become worse in the days after a crash. Getting checked out promptly protects both your health and your ability to access insurance benefits.

The Emergency Medical Condition Requirement

To access the full $10,000 in PIP benefits, a licensed medical provider must determine that you have an emergency medical condition. If you do not receive that diagnosis, your PIP benefits may be capped at $2,500.

Insurance companies may dispute whether your injuries qualify, whether your treatment was necessary, or whether your condition was caused by the accident. Proper medical documentation matters from the beginning.

What PIP Covers

PIP may help pay for several accident-related expenses, including:

- Emergency room treatment

- Ambulance transportation

- Doctor and specialist visits

- Diagnostic imaging, including X-rays, MRIs, and CT scans

- Surgery

- Physical therapy and rehabilitation

- A portion of lost wages

However, PIP does not cover everything. It does not pay for pain and suffering, and it does not cover vehicle damage. It also usually leaves a 20% gap in medical expenses, along with any deductibles or bills that exceed your policy limits.

What Happens When PIP Is Not Enough?

When PIP runs out, other payment sources may become important. The options available depend on your insurance policy, the at-fault driver’s coverage, and the severity of your injuries.

MedPay Coverage

Medical Payments Coverage, or MedPay, is optional in Florida. If you have it, MedPay may help cover medical expenses beyond PIP. It can also help pay the 20% of bills that PIP does not cover.

Health Insurance

If your PIP and MedPay benefits are exhausted, your health insurance may cover ongoing treatment. This may include private health insurance, Medicare, or Medicaid.

However, health insurers may have reimbursement rights. This means they may seek repayment from your eventual settlement for accident-related medical expenses they covered. A Pensacola car accident attorney can help review and negotiate those claims so they do not unfairly reduce your recovery.

The At-Fault Driver’s Insurance

The at-fault driver’s insurance company usually does not pay your medical bills one by one as they arrive. Instead, those expenses are typically addressed later through a settlement or lawsuit.

If the at-fault driver has bodily injury liability coverage, that policy may help pay for medical expenses, lost wages, pain and suffering, and other damages beyond your PIP benefits. However, your injuries may need to meet Florida’s serious injury threshold before you can pursue certain damages from the at-fault driver.

Uninsured and Underinsured Motorist Coverage

If the driver who hit you has no insurance or does not have enough coverage, your own uninsured/underinsured motorist coverage may apply. UM/UIM coverage is optional in Florida, but it can be extremely valuable after a serious crash.

Be Careful with Early Settlement Offers

Insurance companies know that medical bills create pressure. If you are hurt, missing work, and worried about paying for care, a quick settlement check can sound like a relief.

But early offers are often made before you know the full cost of your injuries. Once you accept a settlement and sign a release, your case is usually over. If your doctor later discovers that you need injections, surgery, or months of physical therapy, you typically cannot go back and ask for more money.

Before founding Fenimore Injury Law, Michael Fenimore spent five years representing insurance companies and Fortune 500 corporations. He understands how insurers evaluate claims, limit exposure, and use financial pressure against unrepresented accident victims.

Medical Liens and Letters of Protection

Some accident victims need treatment but cannot afford the out-of-pocket costs. In certain cases, medical providers may agree to treat a patient through a medical lien or Letter of Protection.

Under this type of arrangement, the provider agrees to wait for payment until the case resolves. When a settlement or verdict is paid, the provider is paid from those proceeds.

This can help injured people continue treatment while their case is pending, but liens must be handled carefully. If they are not reviewed or negotiated, they can significantly reduce the final recovery.

How Medical Bills Are Handled in a Settlement

When a car accident case settles, the settlement may need to account for several expenses before the client receives the final net recovery. These may include:

- Outstanding medical bills

- Medical liens

- Health insurance reimbursement claims

- Medicare or Medicaid reimbursement issues

- Attorney’s fees and case costs

An attorney can often negotiate with medical providers and lienholders to reduce the amount owed. This can make a significant difference in how much money the injured person actually receives after the case resolves.

Steps to Protect Yourself After a Pensacola Car Accident

- Seek medical treatment within 14 days of the crash.

- Tell your providers that your injuries came from a car accident.

- Follow your treatment plan and avoid gaps in care.

- Keep all medical bills, records, receipts, and insurance statements.

- Notify your auto insurer promptly.

- Do not sign a settlement release until you understand the full extent of your injuries.

- Review your policy to see whether you have MedPay or UM/UIM coverage.

- Speak with a Pensacola car accident lawyer if your bills are mounting or the insurance company is pressuring you to settle.

How Fenimore Injury Law Helps with Medical Bills After a Car Accident

You should not have to spend your recovery trying to untangle insurance coverage, billing departments, medical liens, and settlement calculations on your own.

Fenimore Injury Law helps Pensacola car accident victims understand how their medical bills may be paid and how those expenses fit into the larger injury claim. We communicate with insurance companies, coordinate with medical providers, review bills and liens, and pursue compensation that reflects both current and future medical needs.

We do not run a high-volume case mill where clients are treated like file numbers. We provide hands-on representation focused on protecting your health, your finances, and your future.

Our firm handles car accident cases on a contingency fee basis. That means there is no upfront fee and no attorney’s fee unless we recover compensation for you.

Speak with a Pensacola Car Accident Lawyer Today

If you were injured in a car accident in Pensacola and medical bills are starting to pile up, do not wait until the insurance company controls the conversation.

A free consultation can help you understand which insurance coverage may apply, whether the at-fault driver may be responsible, and what steps you should take next.

Call Fenimore Injury Law at (850) 434-6064 or fill out our online form to schedule a free, no-obligation case evaluation. Whether you are recovering at home in Pensacola, Gulf Breeze, Pace, Escambia County, or Santa Rosa County, our team is ready to help you take control of your recovery.